Many first-time home buyers are at a stage in their lives where they are also either newlyweds or soon-to-be newlyweds. The cost of paying for your first home while also covering the expenses of a wedding can be financially overwhelming or impossible for some, especially as both have sharply risen in recent years.

According to The Knot, the national average cost of a wedding in 2023 was $35,000 – a $5,000 increase from 2022, while, according to the National Association of Realtors (NAR), the national median single-family home price increased from $402,500 in Q2 2023 to $422,100 in Q2 2024.

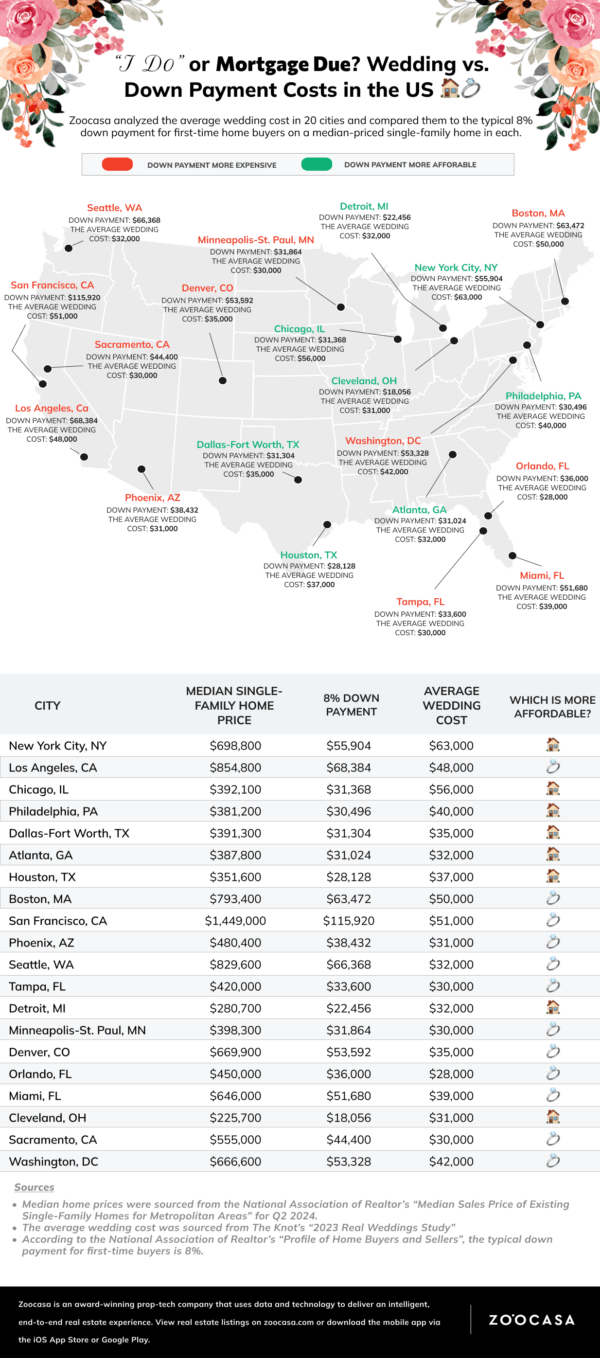

As costs continue rising, many couples may be forced to choose between saving for their dream wedding or saving for their dream house. To help couples better weigh the costs of saying “I do” and putting down a down payment, Zoocasa analyzed the average wedding cost in 80 cities, using data from The Knot, and compared them to the typical 8% down payment for first-time home buyers on a median-priced single-family home.

According to NAR’s 2023 Profile of Home Buyers and Sellers, the typical down payment for first-time buyers is 8%. The Knot calculated the average wedding cost for the top 20 major markets specifically for each city, while the average for the remaining 60 cities was based on their respective state.

Should You Skip the Ceremony and Buy a House?

In 47 of the 80 cities analyzed, the cost of a down payment is actually lower than the average wedding cost. So for couples who aren’t that enthusiastic about a large celebration, it may be worth considering skipping the ceremony and using the wedding money toward a down payment instead.

In several cities with median single-family home prices below the national median, such as Philadelphia, Houston, and Cleveland, couples could save close to $10,000 by opting for a home instead of a wedding. For example, the average wedding in Philadelphia costs $40,000, while the median price for a single-family home is $381,200. For first-time homebuyers, this means an 8% down payment would amount to $30,496.

In New York City, where the average wedding costs $63,000, a couple could choose to put this amount toward a down payment instead. After covering the typical 8% down payment of $55,904, they would still have $7,096 left over.

However, weddings are not always more expensive than down payments. In some cities, like Orlando, the average wedding costs $28,000—half of what it is in New York City. Meanwhile, the median price for a single-family home in Orlando is $450,000, which brings the 8% down payment to $36,000—$8,000 more than the average wedding cost in the city.

Likewise, Utah, Nebraska, Oklahoma, and Missouri have average wedding costs under $30,000, meaning marriage is likely the more affordable option in cities in these states. This is especially true in Utah, which has the lowest average wedding cost in the U.S. For just $17,000, couples in Utah can hold a wedding ceremony, but if they plan to live in Salt Lake City or Provo, they’ll need to save over $40,000 for a down payment.

Huge Price Gaps Between Weddings and Down Payments

The difference in cost between a wedding and a down payment can be astronomical in some cities. San Francisco is one of the most jarring examples of this as the city has one of the country's highest median single-family home prices. At $1,449,0000, an 8% down payment would come out to $115,920, which is more than double the average wedding cost of $51,000.

Chicago is the exact opposite; median single-family home prices are relatively lower compared to other large cities, while the average wedding cost is the second-highest on the list. This results in the 8% down payment being $24,632 less than the average wedding cost of $56,000. However, if couples opt for a wedding in the Chicago suburbs, they could save some money as the average wedding cost there is only $35,000.

Where the Cost of a Wedding and Down Payment are Similar

As average annual household expenses continue to rise—up 5.9% from 2022 to 2023 according to the latest U.S. Bureau of Labor Statistics data—couples will need to think carefully about their financial priorities when deciding between holding a large ceremony and investing in property. This is particularly relevant in cities and states where the cost of a wedding and down payments are similar.

According to the Federal Reserve’s 2022 Survey of Consumer Finances, the average American renter has $16,930 in savings while the average American under $35 has $20,540. This means it’s likely that many couples will struggle to be able to afford both a wedding and the purchase of a home.

In Atlanta, for instance, the average wedding cost is $32,000, while the typical 8% down payment on a median-priced home comes out to $31,024. With less than a $1,000 difference between these two significant expenses, financial prioritization becomes more crucial than ever. Indianapolis, Kansas City, Tucson, and Des Moines are some of the other cities with less than a $1,000 difference between a wedding and a down payment.

Can Couples Afford Both a Marriage and a Mortgage?

Buying your first home and holding a wedding are two of the largest expenses in your life, but there are ways to lower these costs and afford them both. For one, if you live in a state that has higher average wedding costs, such as New York or New Jersey, you could opt to have a destination wedding in a more affordable location, both in the US or abroad. The average cost for a domestic destination wedding is $43,300 according to The Knot, which is still below the state averages for New York and New Jersey.

Couples could also choose to invite fewer people, as the average wedding with 1-50 guests is just $16,700, or cut back on vendor costs. For instance, the average cost of a live band is $4,300, whereas the average cost of a DJ is only $1,700.

To save money on their first home, couples might consider purchasing a condo. This allows them to build equity over a few years before upgrading to a single-family home. In many cities, including Houston, Columbus, Jacksonville, New Orleans, and Philadelphia, the median price of a condo remains below $300,000, making it a more affordable entry point into homeownership.

Do you have questions about buying your first home? Give us a call today to discuss your home-buying plans with one of our qualified agents.