A beachfront escape or a European getaway sounds tempting, but what if that vacation budget could be the key to homeownership instead? With rising living costs and growing concerns about housing affordability, many Canadians are reassessing their financial priorities.

For some, skipping an annual vacation, an expense that averaged $4,241 per traveler in the past year, according to a 2024 Blue Cross Travel Study, could make a meaningful dent in a down payment. But how long would it take to turn travel savings into home equity?

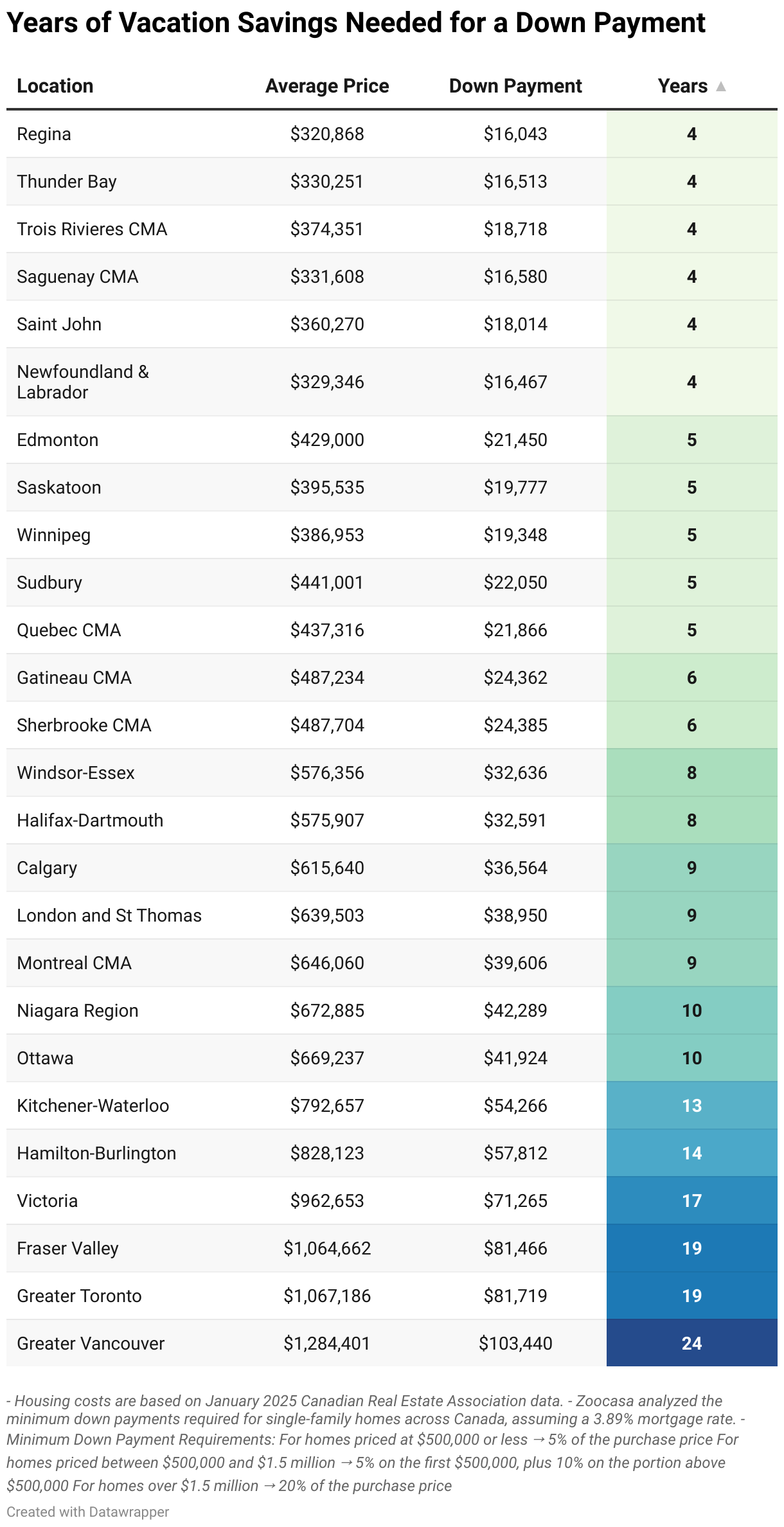

To answer that, Zoocasa analyzed the minimum down payments for single-family homes across Canada, using a 3.89% mortgage rate—one of the lowest currently available, according to Ratehub. By comparing home prices to annual vacation costs, we calculated how many years of forgoing travel it would take to reach homeownership.

The Fast-Track to Homeownership

In some regions, four years of redirecting vacation funds could be enough to secure a down payment. If you’re looking to buy in Regina, Thunder Bay, Trois-Rivières, Saguenay, Saint John, or Newfoundland and Labrador, skipping a big trip each year could get you into homeownership in approximately the same time it takes to earn a university degree. In these regions, saving less than $4,500 per year could be a significant head start on owning a home.

Cities Where Homeownership Requires a Manageable Sacrifice

In Saskatoon, Edmonton, Winnipeg, Sudbury, and Quebec City, accumulating a solid down payment would take five years of skipped vacations. Meanwhile, Gatineau and Sherbrooke require slightly longer at six years. While giving up vacations may seem challenging, it’s a relatively short-term sacrifice for long-term stability.

Overall, half of the Canadian cities analyzed require six years or less to save for a down payment, making homeownership a realistic goal, especially for people without debt. Combining this strategy with other savings efforts, such as living with roommates longer, picking up a side hustle, or cutting non-essential expenses, could further reduce the timeline.

The Long Haul: Cities Where Saving a Down Payment Takes Nearly a Decade

In this example, saving a minimum down payment means forgoing vacations for eight years for aspiring homeowners in Windsor-Essex and Halifax-Dartmouth. In Calgary, London-St. Thomas and Montreal’s timeline stretches to nine years, a significant commitment for those eager to enter the housing market.

While skipping nearly a decade of travel may seem overwhelming, there are ways to accelerate homeownership without completely sacrificing lifestyle. If five years of vacation savings can cover half a down payment, pairing this with strategies like house hacking, investing, or purchasing a more affordable starter home could fast-track your journey while allowing occasional getaways.

The trade-off for those set on buying in Ottawa is even greater: 10 years of vacation savings would be needed to reach a minimum down payment. That’s a long road, but considering smaller secondary markets first could be a better way to start investing. Building equity in a more affordable city before transitioning to a pricier one can provide a more realistic and sustainable path up the property ladder.

15+ Years in Canada’s Most Expensive Cities

For those looking to buy in Victoria, Fraser Valley, Toronto, or Vancouver, the path to homeownership is much steeper. Homebuyers must forgo vacations for at least 15 years in these cities to save a minimum down payment. Vancouver stands out as the most challenging market, requiring a staggering 24 years of savings and nearly a lifetime of missed trips to reach the starting line of homeownership.

Given these extreme timelines, a more practical strategy is to start with a condo or apartment in a smaller, more affordable market. By purchasing a lower-cost property over a single-family detached, homeowners can build equity over time, eventually using that accumulated value to transition into a larger home in a pricier city.

Timing also plays a crucial role. Waiting for a period of high condo inventory can increase the chances of finding a good deal. When supply outpaces demand, prices often stabilize or drop, making it easier to enter the market without overextending financially. Patience and market awareness can turn an overwhelming housing challenge into a more attainable goal.

Reframing the Vacation vs. Down Payment Debate

Skipping vacations isn’t the only way to fast-track homeownership. Many Canadians are choosing a hybrid approach—buying in more affordable markets (with a five-to-six-year savings timeline) to build equity while still taking occasional trips. This strategy allows for both financial growth and meaningful life experiences.

If going a decade without vacations feels overwhelming, consider alternatives like staycations or working abroad. This way, you can experience new places while progressing toward your educational and investment goals.

Overall, homeownership and travel don’t have to be an either-or decision. With the right financial plan, you can have both home keys and passport stamps in your future.