With inflation reaching historic peaks across the country, the Bank of Canada has confirmed they are considering raising their Overnight Lending Rate, the trend-setting rate that sets the tone for the interest rates consumers will see on new lines of credit, credit cards, and mortgages, in the second quarter of 2022.

The Overnight Lending Rate has been at a record low of 0.25% since the start of the COVID-19 pandemic to help support the economy throughout the pandemic. Lowering interest rates to keep money moving in uncertain times is a strategy used by many central banks, in the United Kingdom and the United States, and has been an important part of global economic recovery from the pandemic. However, now that vaccine rollouts have stabilized many national economies from the threat of COVID-19, interest rate increases are being considered in many countries to combat inflation.

With interest rate hikes on the horizon, many Canadians are keeping a close eye on the housing market. While it’s undeniable that an increase in interest rates will make the cost of mortgage borrowing more expensive, it’s unclear if these rate hikes will do anything to cool the country’s red-hot housing market that’s been breaking records for sales and price appreciation since interest rates were lowered at the start of the pandemic.

Related Read: Bank of Canada Holds Rate Firm In Their Final Step Of Exiting From Emergency Policies

To help understand what could be in store for 2022, Zoocasa has taken a historical look back at what happened when the Bank of Canada raised its Overnight Lending Rate in 2018 to help understand the relationship between rate increases and the real estate market.

Understanding Toronto’s Real Estate Market in Relation to Canada’s Economy in the late 2010s

The last time the Bank of Canada raised their Overnight Lending Rate was in 2018, with three hikes of 0.25% throughout the year. Coupled with an earlier hike of 0.25% in August of 2017, the central bank raised rates 1% in a little over a year. By the end of this increase cycle, the Overnight Lending Rate was 1.75%, the highest rate recorded in the 2010 decade.

These rate increases followed a small series of decreases in 2015, after a slowdown in oil and gas prices led to uncertainty in Canada’s economy. The effects of this economic downtown were felt most strongly in the prairies, while the economy in most other provinces remained steady.

From a real estate perspective, the mid-2010s saw significant upwards pressure on pricing. However, this growth was highly regionalized, with larger cities like Toronto and Vancouver seeing the most significant price appreciation. Vancouver was the most expensive of the two cities, with prices increasing sharply in the latter half of 2015 – with detached homes increasing by an average of $420,000 in a five-month period.

This red-hot appreciation prompted regional policy action, and British Columbia implemented a 15% Foreign Buyer’s Tax in 2016. However, it’s theorized that Vancouver’s implementation of the tax only pushed foreign investors into Ontario’s market, with the largest gains in demand happening outside of Toronto in the 905 markets. This led to red-hot price growth throughout the end of 2016 into 2017 in the GTA with prices growing nearly 25% year-over-year when comparing April of 2016 and 2017.

In 2017, government policy was introduced at both the federal and municipal levels to cool the housing market and protect the overall Canadian economy. Most notably, the Ontario Fair Housing Plan, which included a 15% Foreign Buyer Tax, was implemented in April of 2017, and the Federal Stress Test, which was introduced in October of 2017 and implemented at the start of 2018.

Shortly after the government announced these policy changes, the Bank of Canada began their most recent increase schedule, citing that country’s economy has adjusted to lower oil prices and has strengthened since their fall as the reason to increase rates.

What impact did Overnight Lending Rate changes have on the housing market?

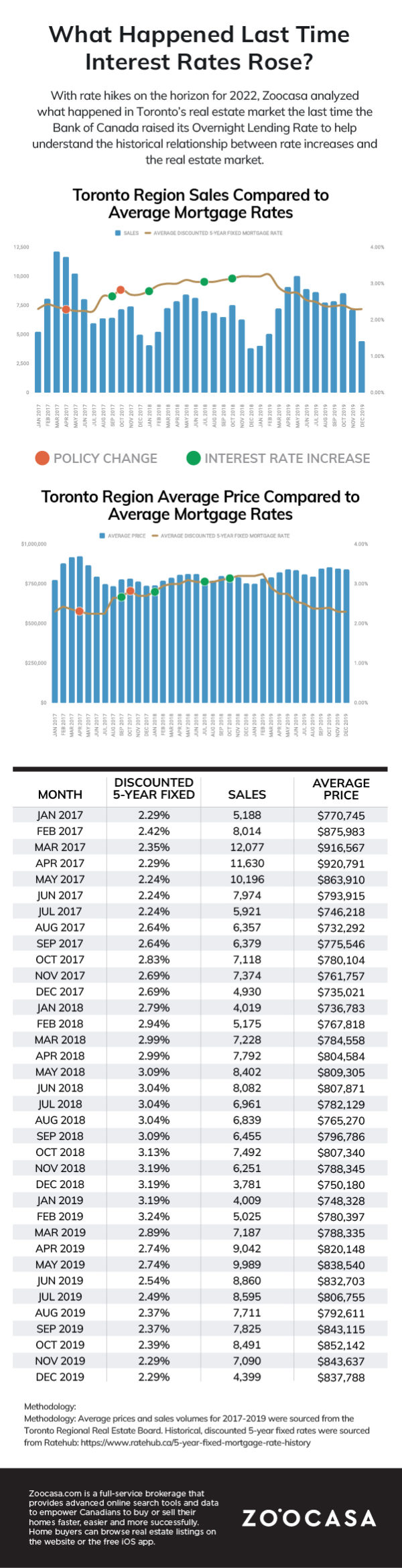

To understand the impact of the Central Bank’s most recent rate increases on the housing market, Zoocasa compared the monthly average home price and sales volumes from 2017-2019 against the average discounted 5-year fixed mortgage rate during that same period, to track any correlations between changing costs of borrowing and the housing market. The average discounted 5-year fixed mortgage rate was charted in lieu of the trending Overnight Lending Rate, since this is the rate that consumers will interact with more closely.

Notable events, like changes to the Overnight Lending Rate or new policy announcements, were also tracked on the chart to help identify how these changes interacted with the housing market.

Policy changes carried the most weight when it came to cooling the market

Out of the three years studied, it’s clear that the largest price and sale decreases had nothing to do with the Bank of Canada’s increase schedule. Promptly after the Government of Ontario introduced the Ontario Fair Housing Plan in April of 2017, prices growth and sales halted.

In the three months following the implementation of the Fair Housing Plan, prices dropped over 20% from their peak in April across the GTA – reducing the average price of a home by more than $100,000 in the Region. Although the decrease was felt across the Region, certain markets were impacted more than others. Values in Richmond Hill, one of the areas with the highest concentration of foreign investment at that time, had average values decrease over $250,000 in just a month.

Interest rate increases seemed to correlate to slower sales numbers, but no major impact on prices

2018 saw the lowest total number of sales in recent memory, with only 78,018 transactions over the course of the year. However, it’s more likely that the Stress Test, which reduced buyers’ budgets by an estimated 20% was more impactful in slowing the market throughout the year.

“Higher borrowing costs coupled with the new mortgage stress test certainly prompted some households to temporarily move to the sidelines to reassess their housing options. With this said, it is important to note that market conditions were improved in the second half of [2018], both from a sales and pricing standpoint,” explained former TRREB President, Garry Bhaura, when recapping the GTA market that year.

When it comes to prices, although there were seasonal, monthly variations throughout the rate hike period in late 2017 through 2018, prices remained relatively stable during this time. A year after the first rate hike in September of 2017, prices had ended up relatively flat, up only 2.74% year-over-year.

When closely examining how prices fluctuate in the months after the interest rate changes, we can see that directly after the rate hikes there were very small movements on the average price, which could be just as easily attributed to seasonal variation as much as the rate hikes themselves.

For instance, the largest month-over-month price drop after an interest rate announcement in the period studied was November 2018, when prices decreased 2.35% following the October announcement. The largest increase was in February of 2018, when prices grew 4.21% after the January announcement. In both cases, these monthly decreases and gains are fairly similar to the pricing trends observed in 2017 and 2019, suggesting that any immediate changes could be attributed to seasonality.

In summary, rate hikes are a sign of economic change, and the uncertainty associated with them seems to cause potential buyers and sellers to wait before getting into the market – leading to a reduction in sales, but not necessarily a reduction in average price.

What does this mean for 2022?

Although the Bank of Canada has announced they’d consider raising rates as early as Q2 of this year, the Bank is closely watching the Canadian economy to determine when the right time to raise rates will be. Factors like COVID-19 recovery, inflation, the overall economic health of the country, and the larger geopolitical landscape all play an important role in their decision to raise interest rates.

When it comes time for interest rates to rise, it’s important for Canadians to consider that the Stress Test was put in place to ensure that Canadians who purchased a home during our historically low rate period would still have an appropriate debt-to-servicing ratio if interest rates increased – so many households should have a built-in buffer in their budgets.

Not to mention, if you have a fixed-rate mortgage, you won’t be paying a higher mortgage rate until it’s time to renew your term. And, even if you signed on for a variable term, depending on the details of your mortgage agreement, your monthly payment might not change (instead, the amount you’re paying in interest could fluctuate).

The next Bank of Canada will be telling Canadians whether they’ve decided to raise their Overnight Lending Rate in their next announcement, scheduled for March 2nd. Sign up for the Zoocasa Newsletter to find out more about their announcement, and what it could mean for the housing market, once it’s released.

For more information on this report, or to arrange for media commentary, please contact communications@zoocasa.com

METHODOLOGY: Average prices and sales volumes for 2017-2019 were sourced from the Toronto Regional Real Estate Board. Historical, discounted 5-year fixed rates were sourced from Ratehub: https://www.ratehub.ca/5-year-fixed-mortgage-rate-history