Saving money for a down payment on a home ranks among individuals’ most important financial goals. However, determining a realistic savings target becomes more complex when considering associated closing costs. For example, in addition to the down payment and land transfer taxes, several other factors may influence the total cash required for purchasing a home, including provincial sales tax (PST) on mortgage insurance, lawyer fees, and title insurance.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

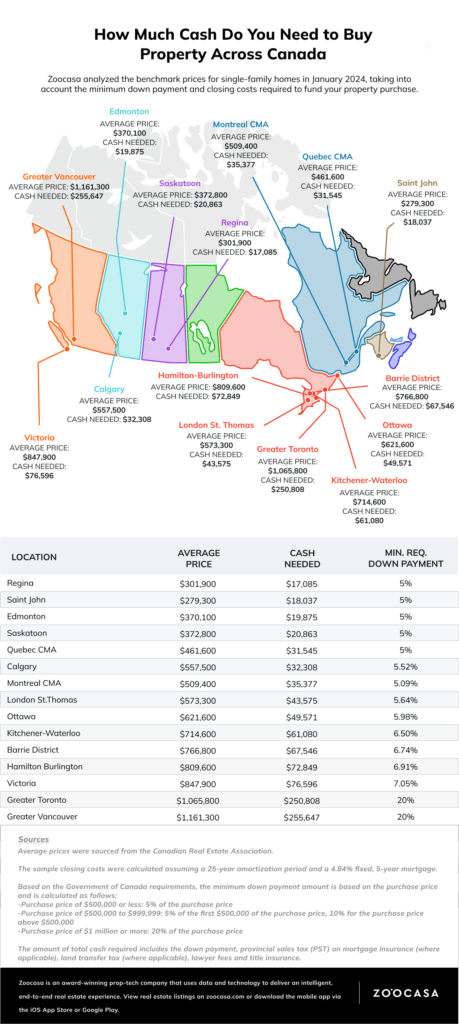

Zoocasa analyzed composite January 2024 benchmark prices for single-family homes sourced from the Canadian Real Estate Association within 15 housing markets while including the additional mandatory costs highlighted above.

It’s important to note that our approach follows Canada’s federal regulations regarding down payments for property structures depending on price. Additionally, the figures are based on a standard 25-year amortization period and a fixed mortgage rate of 4.84%, and our calculations offer a comprehensive overview of these costs. Overall, this will provide a clearer understanding of the cash requirements involved.

Navigating Land Transfer Tax in Canada

For Canadian provinces, individuals acquiring land are subject to provincial land transfer taxes upon closing. These taxes, payable in full at closing, must be incorporated into your closing cost preparations.

Alberta and Saskatchewan are the only provinces without a land transfer tax. However, in Saskatchewan, fees associated with registering legal documents apply. Meanwhile, in New Brunswick, the land transfer tax constitutes a flat 1% tax on the assessed property price or its purchase price, whichever is greater.

The municipality you’re purchasing a home in also plays a significant role. For instance, as a Toronto homebuyer for condos and single-family homes, you must pay the provincial Ontario land transfer tax and the municipal Toronto transfer tax.

The Most Affordable Housing Markets for Buyers

Regina is the most affordable place to purchase a single-family home, requiring only $17,085 to save for a down payment and associated closing costs. Saint John also stands out for affordability, with an average home price of $279,300, necessitating $31,545 in cash. Lastly, Edmonton secures a spot in the top three, with $20,863 needed for a home priced at $372,800.

Saving for Property in Victoria, Vancouver and Toronto

The highest cash requirement for property purchase and associated closing costs is in Greater Vancouver, where a buyer needs to save a whopping $255,647 for an average home priced at $1,161,300. Toronto follows closely, with $250,808 needed for a home valued at $1,065,800. For homes below the million-dollar mark, Victoria has an average price of $847,900, requiring homebuyers to save approximately $76,596.

Need help navigating the cost of Canada’s real estate market? Give us a call today to speak with a qualified agent who can guide you on local market conditions, interest rates, and more!