It’s no secret that housing affordability remains an acute challenge for many Canadians – according to a recent survey conducted by Zoocasa, a total of 82% of respondents agree it’s a major issue that has negatively impacted the population.

The pressure has been mounting on the federal government is recent years to take action to improve affordability; all eyes are on whether new measures will be announced in the upcoming budget to be released on March 19. As well, new promises to improve Canadians’ ability to buy real estate will be a key platform for all parties as the next federal election approaches in October, to go along with the existing $40-billion Housing Strategy, which is set to build 100,000 new units over the next 10 years. Most recently, the Canada Mortgage and Housing Corporation announced its intent to provide affordable housing for every Canadian by 2030, prioritizing the 1.6 million people currently considered to be in core housing need.

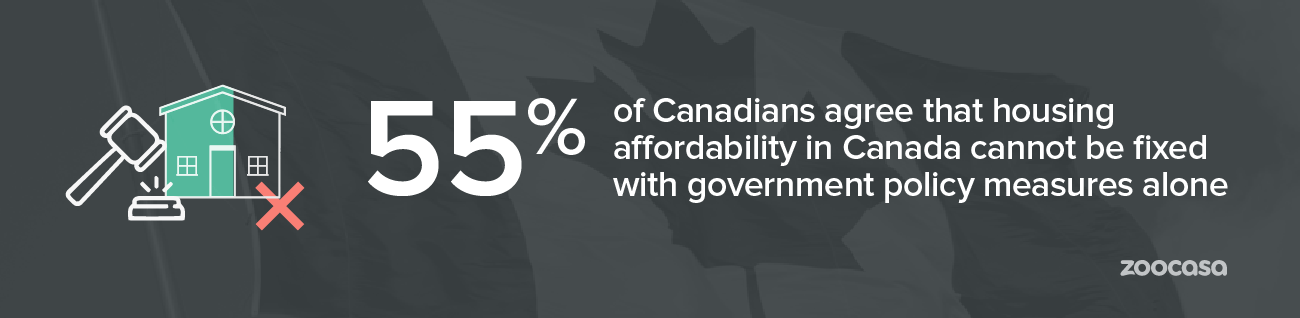

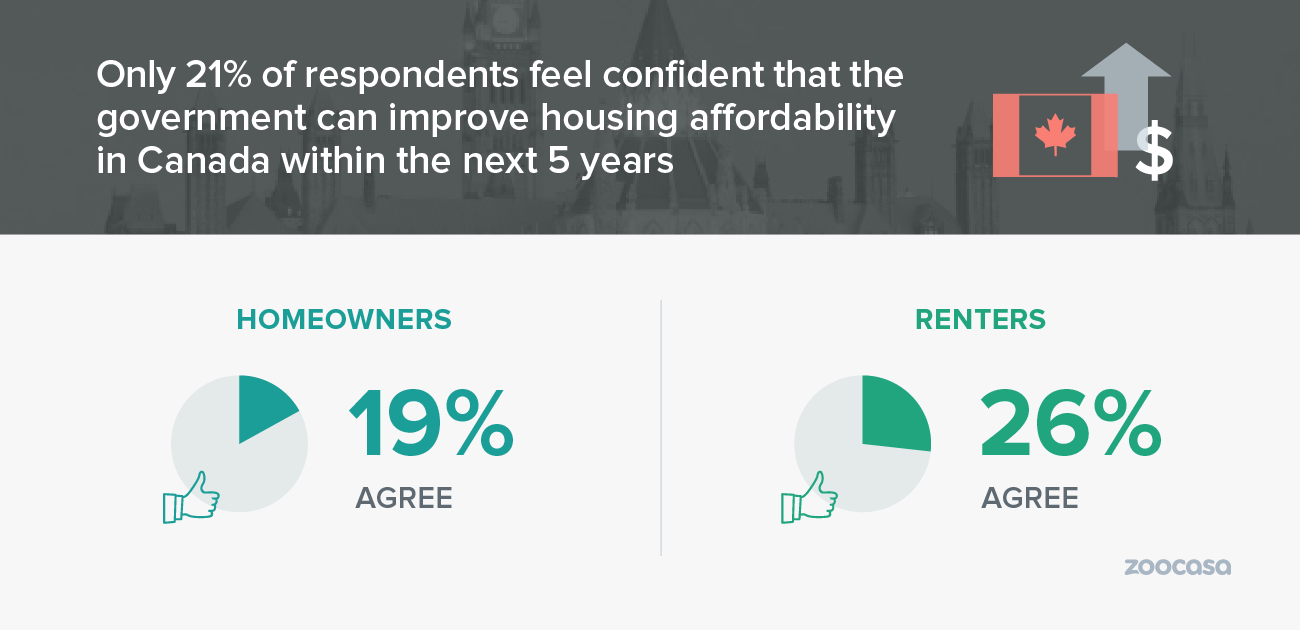

However, the survey, which polled over a thousand respondents, reveals Canadians aren’t overly optimistic about whether government intervention can make a difference; the majority of respondents – 55% – feel that housing affordability in Canada cannot be fixed with government policies alone. In fact, only 21% said they feel confident that the government can improve the situation at all over the next five years.

Real estate associations, analysts, and other bodies have been actively proposing potential measures for the government to include in their budget. While Federal Finance Minister Bill Morneau has alluded a solution of some kind will be announced, it’s not yet clear what form it will take.

Here’s a look at what housing affordability measures could be on the table.

Reducing the Mortgage Stress Test

While there are a number of issues that have impacted affordability, one of the most heavily criticized has been the mortgage stress test. Implemented nationally on January 1, 2018 by the Office of the Superintendent of Financial Institutions, its main purpose is to stem the growth of risky borrowing practices in Canada.

It accomplishes this by requiring new non-insured mortgage applicants, as well as those renewing their terms with a different lender, to prove they could afford a mortgage priced at the Bank of Canada’s benchmark Conventional 5-Year Rate (currently 5.34%), or their lender contract rate plus 2%, whichever is higher. A similar stress has already been in place for borrowers requiring insured mortgages (those who pay 19% or less on their home down payment) since October 17, 2017.

The result has been reduced purchasing power for buyers, which has rippled through all levels of the market; some may have had to downsize their desired home type, exit the market altogether, or explore their options with B and private lenders. This has had a notable effect on housing markets across the nation, including Vancouver homes for sale, which plunged 30% in February, as well as demand for Toronto real estate listings, which softened 2.5% year over year.

That’s prompted a number of real estate organizations, including the Toronto Real Estate Board and Mortgage Professionals Canada, to call for the stress test percentage threshold to be reduced.

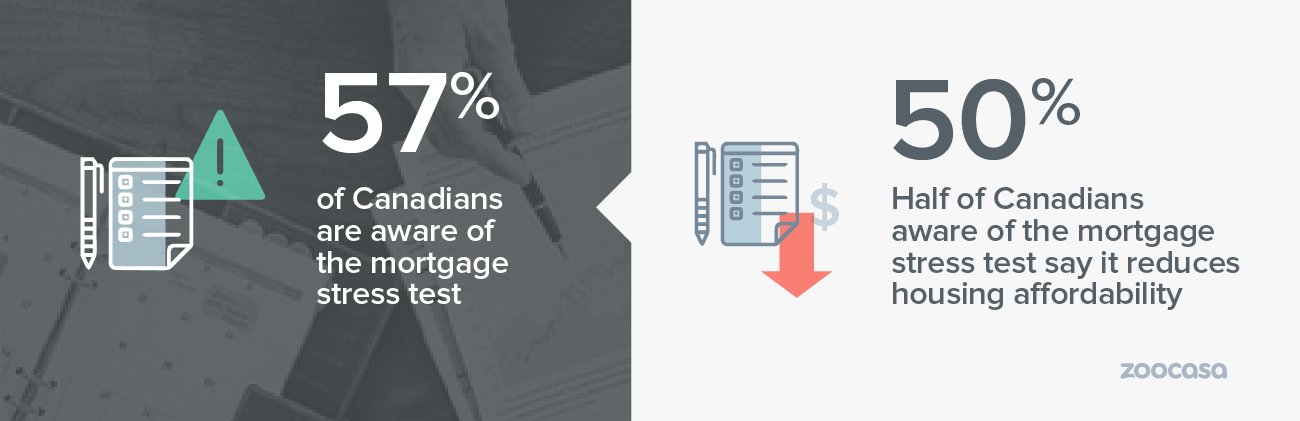

However, the stress test may not be as much of a pain point for consumers as initially thought – only slightly more than half of respondents – 57% – said they were aware of the stress test at all, and of those, 50% said it had reduced housing affordability for Canadians. Perhaps most telling, only 15% indicated that reducing the stress test would be the most helpful measure the government could introduce to help improve affordability.

Increasing the First-Time Home Buyers’ Tax Credit

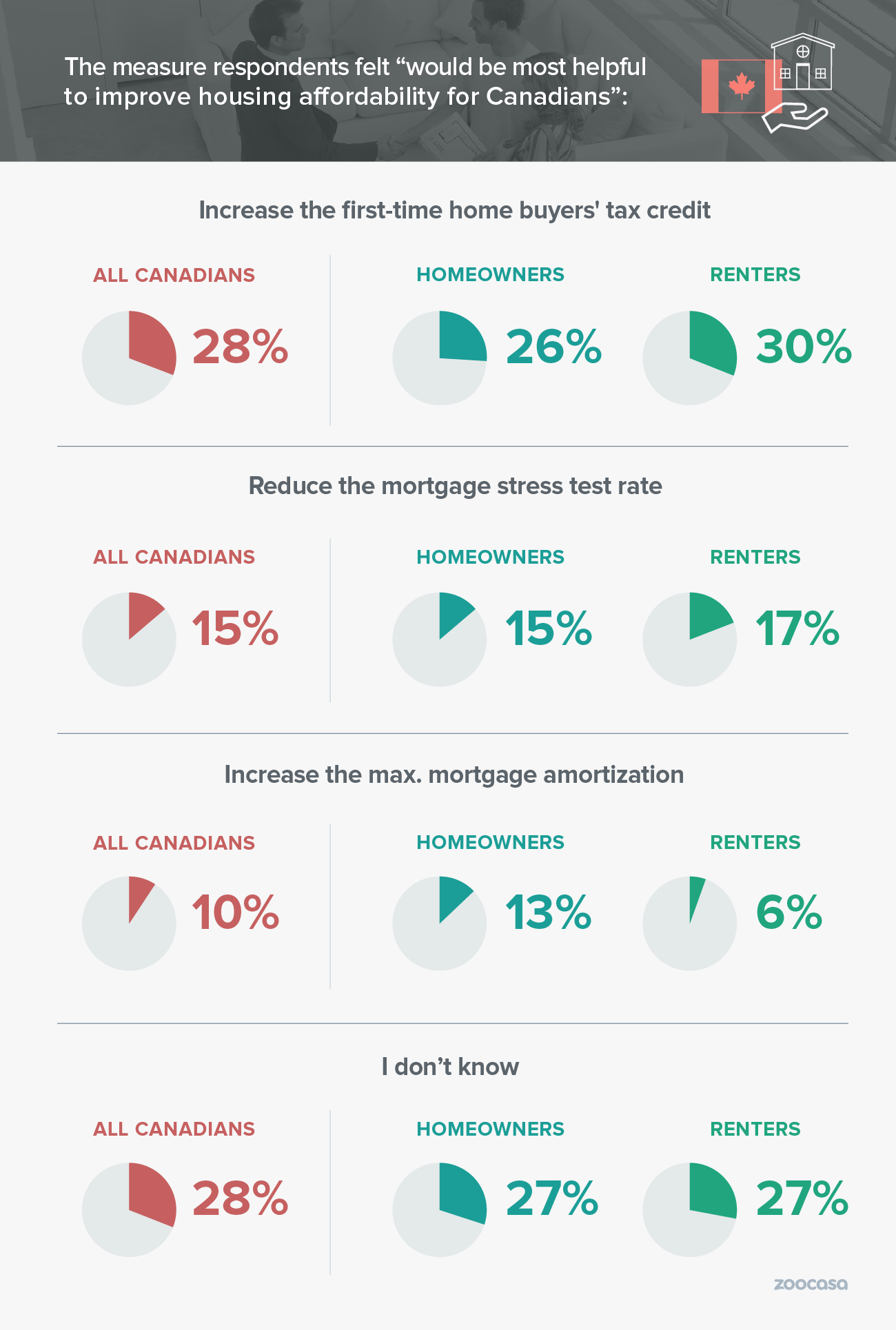

It turns out, Canadians would rather have cash in pocket to aid with their ability to buy a home – a total of 28% of respondents indicated increasing the First-Time Home Buyers’ Tax Credit amount would be the most helpful measure the government could introduce in the budget. Those who identified as renters were slightly more in favour at 30%, while 26% of homeowners agreed.

Currently, first-time home buyers can get a credit valued at $750 when they file their income taxes. The home must be located in Canada and registered to either the

Increasing the Maximum Mortgage Amortization to 30 Years

Another measure that could trim housing costs for buyers would be to extend the length of their mortgage amortization – the total length of time it takes to pay off a mortgage – to 30 years for first-timers. Currently, this option is only available to mortgage borrowers who put 20% down or more on their home purchase, while those under this threshold must pay their home financing back within 25 years.

However, only 10% of respondents indicated this would be the most effective measure to improve housing affordability, with only 6% of renters, and 13% of homeowners in agreeance.

Survey Highlights:

- 82%: The number of respondents who agree housing affordability is a major issue that has negatively impacted Canadians

- 55%: Those who agree housing affordability in Canada cannot be fixed with government policy measures alone

- 21%: Those who feel confident that the government can improve housing affordability in Canada within the next five years. 26% of renters agree, and 19% of homeowners agree

- 57%: Canadians who are aware of the mortgage stress test

- 50%: Of those who are aware of the stress test who feel it reducing housing affordability for Canadians

When asked which measure would be the most helpful in improving housing affordability for Canadians:

- 28%: Increasing the First-Time Home Buyers’ Tax Credit amount. 30% of renters and 26% of homeowners agree

- 15%: Reduce the mortgage stress test rate. 17% of renters and 15% of homeowners agree

- 10%: Increase the maximum mortgage amortization period to 30 years. 6% of renters and 13% of homeowners agree

- 8%: Expand the Home Buyers’ Plan. 8% of renters and 8% of homeowners agree

- 28%: I don’t know

- 11%: None of the above

Methodology

The findings are based on an online survey conducted by Zoocasa.com from March

About Zoocasa

Zoocasa.com is a tech-driven brokerage that empowers Canadians to make more informed real estate decisions. Our proprietary home search tools and streamlined agent experience make buying and selling homes smarter, faster and more successful. Home buyers can browse real estate listings on the website or the free real estate iOS app.

For more information about this report or to set up a media interview, please email communications@zoocasa.com.