After spring, fall is one of the most popular seasons for buying and selling real estate. Following a whirlwind of changes over the past few years, including a global pandemic, fluctuating inflation, shifting interest rates, and a growing trend of people moving away from major cities due to remote work, fall 2024 is shaping to be unique in its own right. Whether you’re looking to buy or sell, this season presents new opportunities in a market that’s evolving once again. Zoocasa used recent Canadian Real Estate Association data to highlight why fall 2024 might be the best market we’ve seen in recent memory.

How Rate Cuts Are Shaping the Fall Market

This fall may be the most advantageous time to purchase a property in years, thanks to the Bank of Canada’s recent reduction in prime rates. After a rapid climb from 2.70% to 7.20% between March 2022 and July 2023, the recent easing of the prime rate is offering buyers a valuable opportunity. Lower rates mean more manageable mortgage payments, making it easier for buyers to qualify for larger loans or reduce financial strain.

For those with variable-rate mortgages, the dip from 6.95% in June to 6.45% in September already provides noticeable relief. Even a small rate cut, like 0.25%, can significantly impact monthly payments, especially for longer-term loans.

With three rate cuts already in 2024, the recent decreases are instilling renewed confidence in the market, especially among individuals hesitant to buy or sell. First-time homebuyers, in particular, may see this as an ideal opportunity to enter the market. After several years of rising interest rates, the ongoing trend of rate reductions creates a more favorable environment for prospective buyers to make their move.

Stable Prices Offer a Clear Path for Buyers

After years of rapid growth, home prices are stabilizing in Greater Vancouver and Greater Toronto, two of Canada’s most expensive markets. In Vancouver, the average home price fell from $1,304,550 in September 2023 to $1,253,823 in August 2024. Similarly, Toronto experienced a slight decline, with prices dropping from $1,119,428 to $1,074,542 over the same period. These figures are especially notable for markets that have seen consistently fast-paced price increases in recent years.

Ottawa exemplifies market price stability, with average home prices showing minimal fluctuation over the years. In September 2021, the average home price was $642,314, rising slightly to $644,364 by September 2022. Prices peaked at $658,931 in September 2023 before settling at $647,604 in August 2024. Ottawa's price stability means buyers can enter the market with more predictability and less concern about rapid price fluctuations. This consistent trend allows buyers to plan their budgets more confidently, knowing they are less likely to face sudden spikes in property values.

High Price Tags With High Rewards This Fall

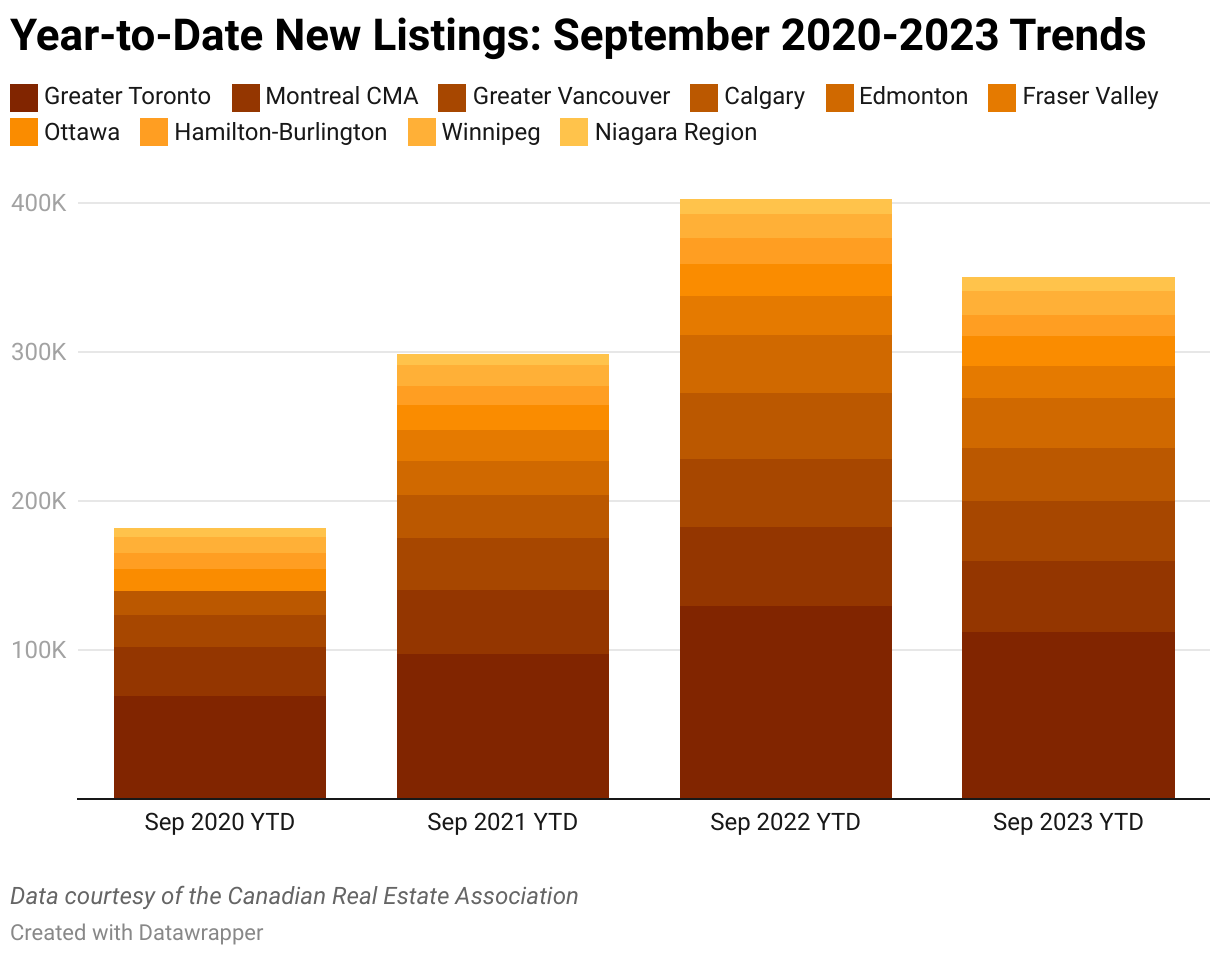

Consider Fraser Valley and Hamilton-Burlington as prime opportunities for solid growth potential. Both regions have seen steady price increases, and with lower interest rates, they present attractive prospects for buyers looking to invest. In Fraser Valley, home prices rose from $842,545 in September 2020 to $1,059,005 in August 2024, showcasing consistent growth and substantial investment potential. Similarly, Hamilton-Burlington saw home prices increase from $722,506 to $886,999 over the same period, positioning it as a prime location for investors as interest rates drop.

Negotiating Power Returns to Toronto Area Buyers

We’ve analyzed August 2024 data from the Canadian Real Estate Association, focusing on the sales-to-new-listings ratio (SNLR) in 26 major markets nationwide. This data was then used to determine August's sales-to-new-listings ratio (SNLR), calculated by dividing the total sales by the number of new listings in each city. The SNLR indicates the level of demand and supply in each area and can thus help local buyers and sellers determine local market conditions.

- An SNLR under 40% suggests a buyer’s market where new listings outweigh sales and buyers have more choice.

- An SNLR between 40% and 60% is a balanced market where demand and supply are at similar levels.

- An SNLR over 60% suggests a seller’s market where demand exceeds supply and sellers have the advantage.

Out of 26 major Canadian real estate markets, only Greater Toronto and the Niagara Region are buyer’s markets, with sales-to-new-listings ratios (SNLR) below 40%.

In Greater Toronto, for example, the SNLR is 39.7%, with 12,547 new listings compared to 4,975 sales.

“As borrowing costs trend lower over the next year-and-a-half, home buyers will initially benefit from both lower monthly mortgage payments and lower home prices. Even as demand picks up, especially in 2025, it will take time for the inventory of listings to be absorbed. Ample choice in the market will help keep price growth moderate, at least in the initial phases of recovery,” Toronto Regional Real Estate Board (TRREB) Chief Market Analyst Jason Mercer stated in the latest market update.

According to the Niagara Association of Realtors President Nathan Morrissette, "Inventory is still holding fairly high, but recent improvement could be a sign of a busier-than-normal end-of-year for Niagara." One of the most influential factors that may be impacting the Niagara Region is that in August 2024, it took an average of 45 days to sell a home, a 36.4% increase from August 2023.

- Related: Concerned About Car Theft? These are the 10 Best and Worst Toronto Neighborhoods for Vehicles

Western Canadian Markets to Watch This Fall

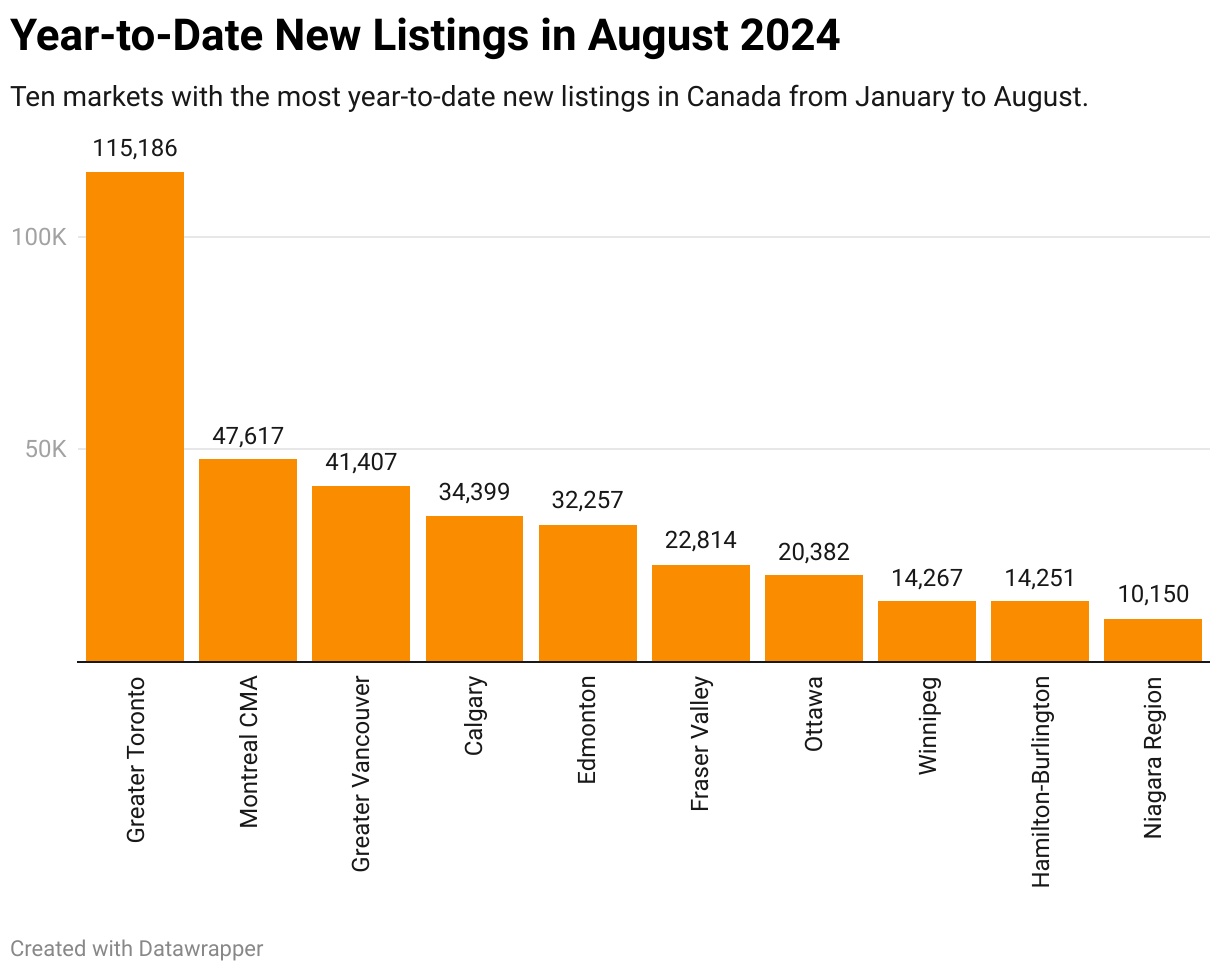

British Columbia, renowned for having the highest housing costs in Canada, is currently experiencing a balanced market in Greater Vancouver, with a sales-to-new-listings ratio (SNLR) of 47.3%. The Greater Vancouver area has seen a decline in year-to-date listings, dropping from 45,819 to 41,407, signaling a shift in available inventory. This is particularly noteworthy given the city's high demand for affordable housing.

“Buyers’ hesitancy to enter the market, paired with new listing activity on the part of sellers that is in line with historical averages, has allowed inventory to accumulate for many months and has moved the market firmly into balanced conditions,” Andrew Lis, Greater Vancouver Director of Economics and Data Analytics said in a press release. "September (is) a month that typically sees an increase in sales from a seasonal perspective, the fall market is set up to bring more buyers off the sidelines.”

Alongside Greater Vancouver, Calgary has emerged as one of Western Canada's most notable markets in recent years, with home prices showing steady growth since 2020. In August 2024, the average home price reached $622,261, a significant rise from $555,694 in September 2023. This follows other significant annual increases, with home prices at $508,011 in September 2022 and $486,519 in September 2021.

So far in 2024, year-to-date new listings in Calgary have reached a whopping 34,399. This marks a substantial increase compared to 16,109 listings in September 2020. The number peaks at 43,990 in September 2022 and slightly decreases to 35,725 in September 2023, reflecting significant growth over recent years.

Ann-Marie Lurie, the Chief Economist at the Calgary Real Estate Board, attributes increased levels of home construction to the gains in new listings, ultimately supporting a better-supplied housing market. “This trend is expected to continue throughout the remainder of the year, but it’s important to note that supply levels remain low, especially for lower-priced properties. It will take time for supply levels to return to those that support more balanced conditions,” Lurie explains in a recent media release.

Are you also looking for a new home this fall? Give us a call today! One of the experienced real estate agents at Zoocasa will be more than happy to help you through the exciting home-buying process.