For those born in the 1990s (a generation that graduated into the 2008 economic recession and hit 30 during the COVID-19 pandemic) the road to homeownership has been anything but smooth. Yet one significant advantage separated some from the pack: whether or not their parents owned property

As reported in a Statistics Canada study titled Housing Statistics in Canada: Parents and Children in the Canadian Housing Market, adults born in the 1990s whose parents were homeowners were twice as likely to own a home in 2021 compared to those whose parents were not. If their parents owned multiple properties, the odds were even stronger—nearly three times higher. The impact was especially significant for those earning under $80,000 a year, highlighting how deeply family wealth now shapes access to housing for a generation hit by back-to-back financial crises. The report also highlights that, among all provinces, British Columbia has the lowest homeownership rate for individuals born in the 1990s, reflecting the impact of Vancouver’s status as the most expensive housing market in Canada.

- Related: GTA Condos That Sold for Under $400K

The Last Decade: A Sharper Decline

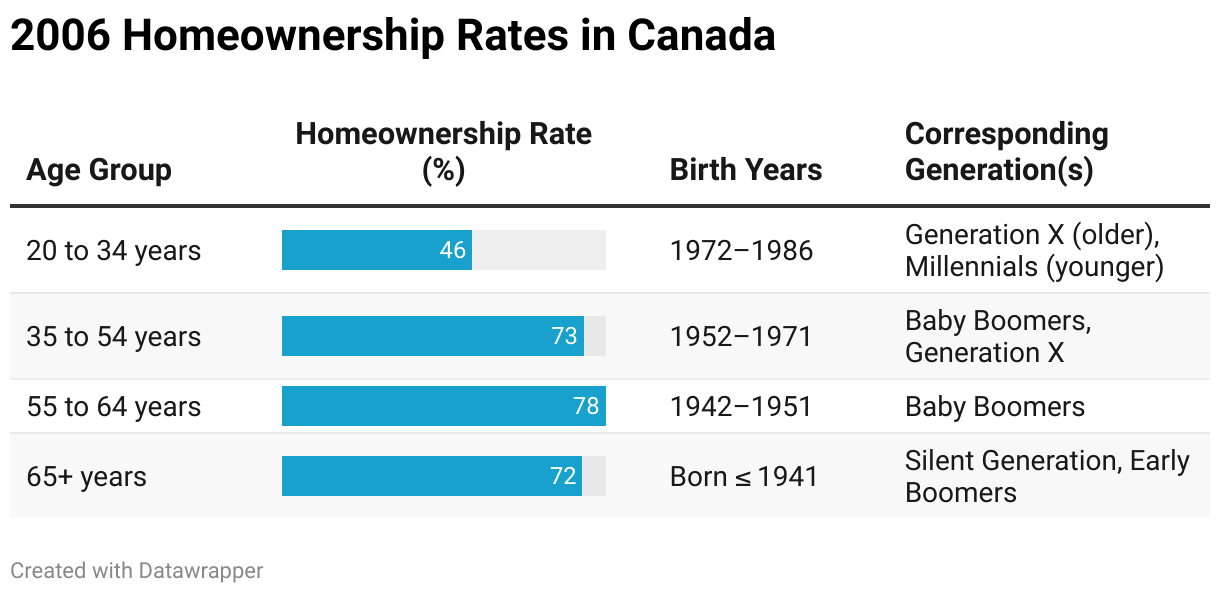

For a while, homeownership remained within reach for young people. In 2006, nearly half (45.7%) of Canadians aged 20 to 34 owned a home. By 2011, the number had even edged up to 47.3%, reinforcing that buying a home shortly after school or early in a career was the natural next step.

But that reality has slipped further out of reach in the past ten years. By 2016, the homeownership rate among 20- to 34-year-olds had dropped to 43.6%, signaling the start of a steeper and more persistent decline.

Despite Canada’s growing population, young adults today are far less likely to own homes than their parents or grandparents were at the same age. By 2021, only 15.5% of adult children born in the 1990s had achieved homeownership. Even among those born in 1990, at 31 years old, only 33% owned homes, a far cry from the nearly 50% ownership rate seen a decade earlier.

More Parents Providing Financial Help

This growing divide between expectations and affordability is why more parents, particularly Baby Boomers and Generation Xers who built significant wealth through real estate, are stepping in to help their children buy homes.

For instance, over the next few years, Canadian baby boomers are expected to pass down a whopping $1 trillion to their heirs, primarily their millennial children. As reported by Ipsos, a survey found that boomers intending to leave 100% of their inheritance to their child(ren) anticipate leaving an average of approximately $960,000. In today’s market, without that kind of family assistance, the once-standard path to homeownership is increasingly out of reach for a generation facing steeper financial barriers.

Consider Millennials born in 1990 specifically. They entered post-secondary school just as North America was recovering from the 2008 financial crisis. Their first jobs came in a shaky market with slow wage growth and rising costs. By 2020, as they turned 30, the COVID-19 pandemic triggered another global financial crisis, affecting every key milestone, including education, career, and homeownership, as well as economic setbacks. For many, the chance to build stability kept slipping further out of reach.

Baby Boomers Hold the Keys to Investment Properties

By 2020, Baby Boomers, those aged 55 and older, had cemented their dominance in the housing market, particularly as property investors. According to a 2020 Statistics Canada report, despite being a minority of the adult population in every province studied, Baby Boomers made up the majority of resident investors: 57.1% in Ontario and 66.9% in Nova Scotia.

The significant presence of Baby Boomers highlights their financial advantages, which stem from decades of higher earnings, stable employment, and opportunities to build wealth.

Unfortunately, younger generations, particularly their now-adult children, find it increasingly challenging to achieve similar financial success. Having benefited from a time when housing was more affordable, Boomers now own a substantial share of investment properties, creating barriers for Millennials and Generation Z as they attempt to enter the housing market.

How Baby Boomer Investors Reshaped Vancouver’s New Home Market

In Vancouver, Baby Boomer investors have significantly transformed the market for newly constructed homes, making it increasingly difficult for younger buyers to access the market. In 1990, the average price of a newly built home in Vancouver was approximately $350,865.

By 2025, this figure is projected to reach an astonishing $2,989,568, representing a whopping increase of over 750% in 35 years.

Boomers were able to enter Vancouver’s new home market when prices were still relatively affordable. In the early 1990s, new builds were priced between $350,000 and $450,000, allowing many to acquire brand-new properties at almost unimaginable costs. As demand surged and land values skyrocketed, new home prices crossed $710,526 by 2006, exceeded $1 million by 2011, and surpassed $2.5 million by 2018.

According to census data by Statistics Canada, in 2000, the median total income for all families in Vancouver was $50,100, while the average price of a newly built home was $419,625 — about 8.4 times the median income. By 2022, the median family income had increased to $109,400, but the average price of a newly built home had soared to $2,604,772, making it roughly 23.8 times the median income. Over this 22-year period, the gap between income growth and home price growth widened significantly, with the home price-to-income ratio nearly tripling.

During this time, Boomers who had already established their presence in the market gained significant equity, which they leveraged to invest further, often purchasing newly built homes as additional properties or investments.

Young Adults Still Hold out Hope

Conversely, Millennials and Gen Z have faced a markedly different market. By the time they were prepared to buy, the entry cost for a new build had become nearly unattainable. Even with declining mortgage rates after the 2008 financial crisis, the gap between incomes and home prices widened.

Currently, at the average price of a newly constructed home nearing $3M, the down payment alone often exceeds the total cost of a new home from a few decades ago.

Despite these challenges, the dream of homeownership is far from extinguished among younger Canadians. According to Scotiabank’s 2024 Housing Study, while more than half of Millennials (55%) and Gen Z (58%) feel that buying a home is out of reach, 58% of Canadians aged 18 to 43 remain determined to achieve this goal within the next five years. Only time will tell how many will be assisted by the Bank of Mom and Dad.