This past September, journalist Katrina Onstad wrote a Maclean’s article, The Jackpot Generation, which explored a significant financial shift Canadians will soon face. Over the next few years, Canadian baby boomers are expected to pass down a whopping $1 trillion to their heirs—primarily their millennial children. “According to an Ipsos survey, boomers planning to leave their entire estate to their children will pass on an average inheritance of $940,000,” the Macleans article states.

This unprecedented wealth transfer will likely reshape the real estate landscape. Millennials will likely use these windfalls to break into a previously unattainable market. Even a fraction of that inheritance can open doors to homeownership or lucrative investment opportunities, particularly when paired with savvy financial planning.

Think of a $200,000 down payment—less than a third of the average $940,000 inheritance. Zoocasa’s calculations, using a 25-year mortgage term and a 3.99% interest rate, showcase how effectively this amount can be leveraged in housing markets across Canada.

Related: Millennial Magnet Cities: Where Young Homeowners Are Taking Root

Ushering in a New Generation of Buyers

For aspiring homeowners, down payments are the power move that sets the stage for long-term success. In Canada’s ever-shifting real estate game, the size of your down payment can mean the difference between just getting by and genuinely thriving, with its impact changing dramatically depending on the market.

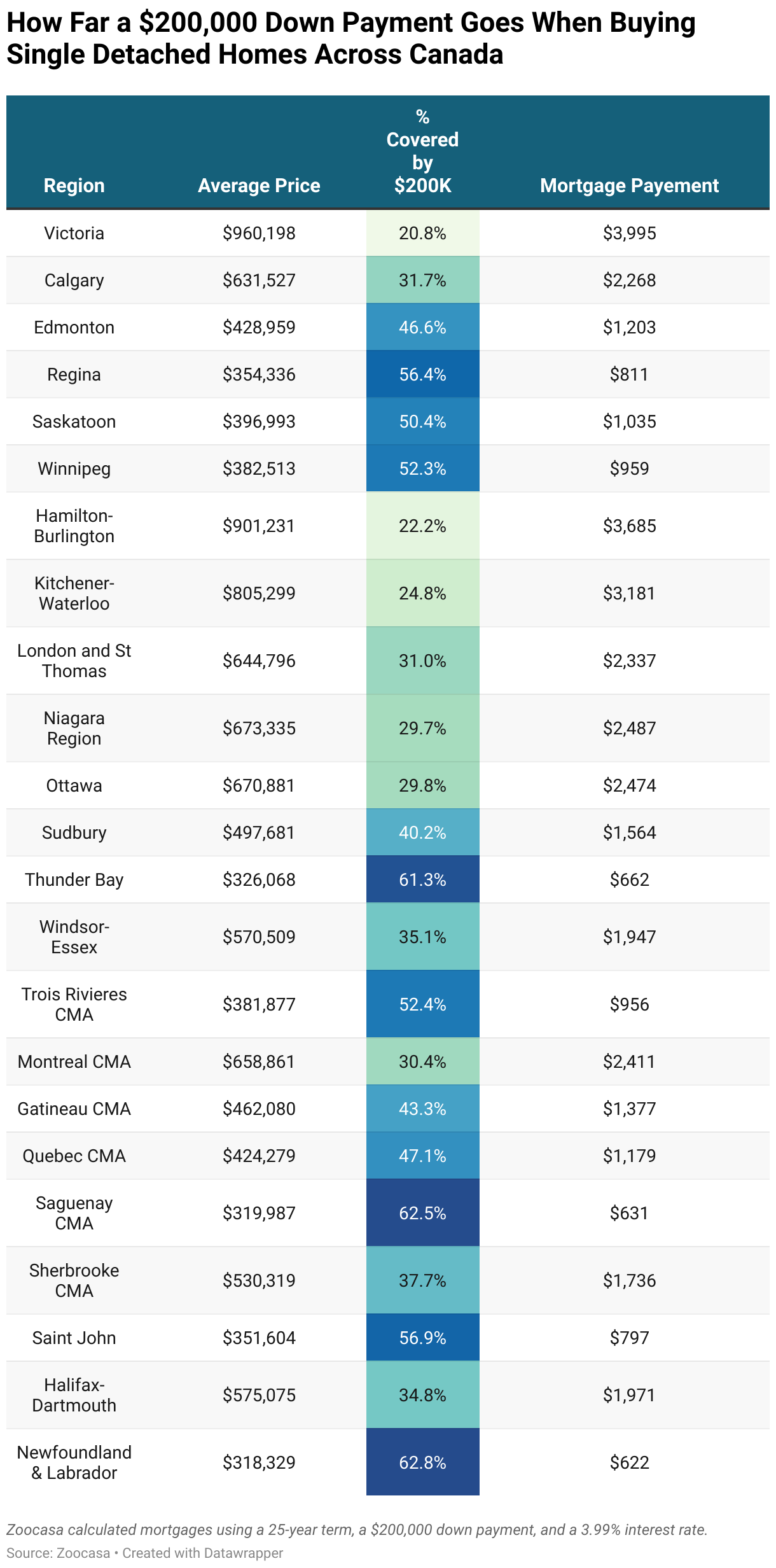

In Calgary, where the average home price is $631,527, a $200,000 down payment covers 31.7% of the total cost, bringing monthly mortgage payments to $2,268. And in Edmonton, the same amount covers nearly 47% of a $428,959 home, slashing payments to just $1,203. These two Western Canadian cities stand out for their affordability, strong rental demand, and long-term growth potential.

Meanwhile, Ontario offers many opportunities, ranging from premium-priced homes in the Greater Toronto Area (GTA) to more budget-friendly options in mid-tier cities. For instance, in Hamilton–Burlington, a $200,000 down payment covers over 22% of the average home price of $901,231, bringing the mortgage balance to $702,960. While the monthly savings may seem modest—about $95 compared to a slightly smaller down payment—it translates into over $1,100 in annual savings. In cities like London, Niagara, and Ottawa, the $200,000 down payment accounts for nearly 30% of a home’s value, reducing monthly payments to $2,000–$2,400.

The math is even more compelling for those eyeing Ontario’s northern markets. In Thunder Bay and Sudbury, that same $200,000 covers 50% of the home’s cost, bringing monthly payments below $1,000—a budget-friendly option with plenty of room for rental profits.

Additionally, the East Coast also offers enticing opportunities for millennial buyers. In Saint John, New Brunswick, where the average home price is $351,604, a $200,000 down payment covers a staggering 57%, leaving monthly payments under $800. Halifax-Dartmouth is another standout, with a $200,000 down payment covering nearly 35% of a $575,075 home and bringing monthly payments below $2,000. Newfoundland and Labrador, with an average home price of $318,329, boasts some of the lowest payments in the country—just $622 a month after applying that hefty down payment.

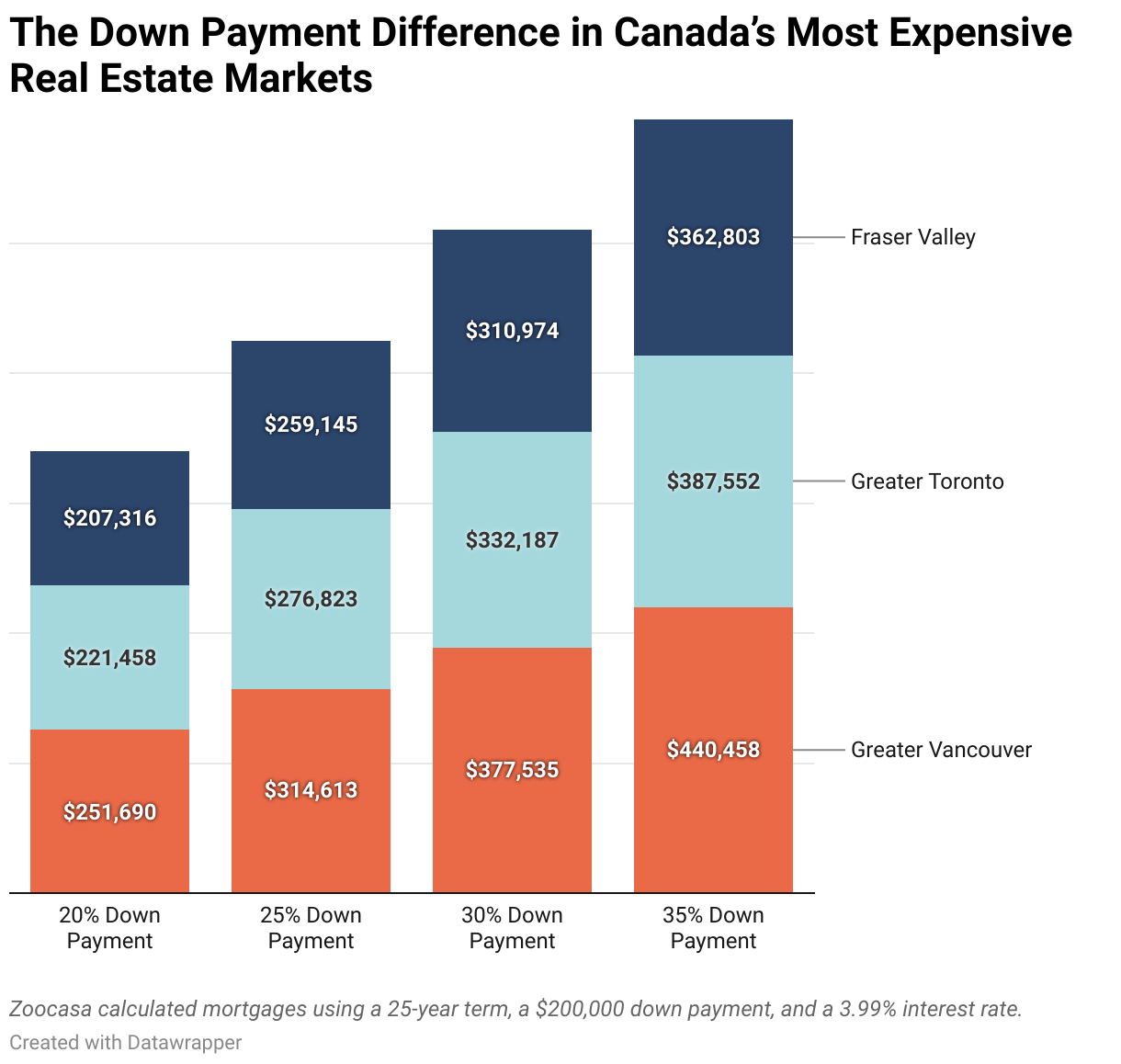

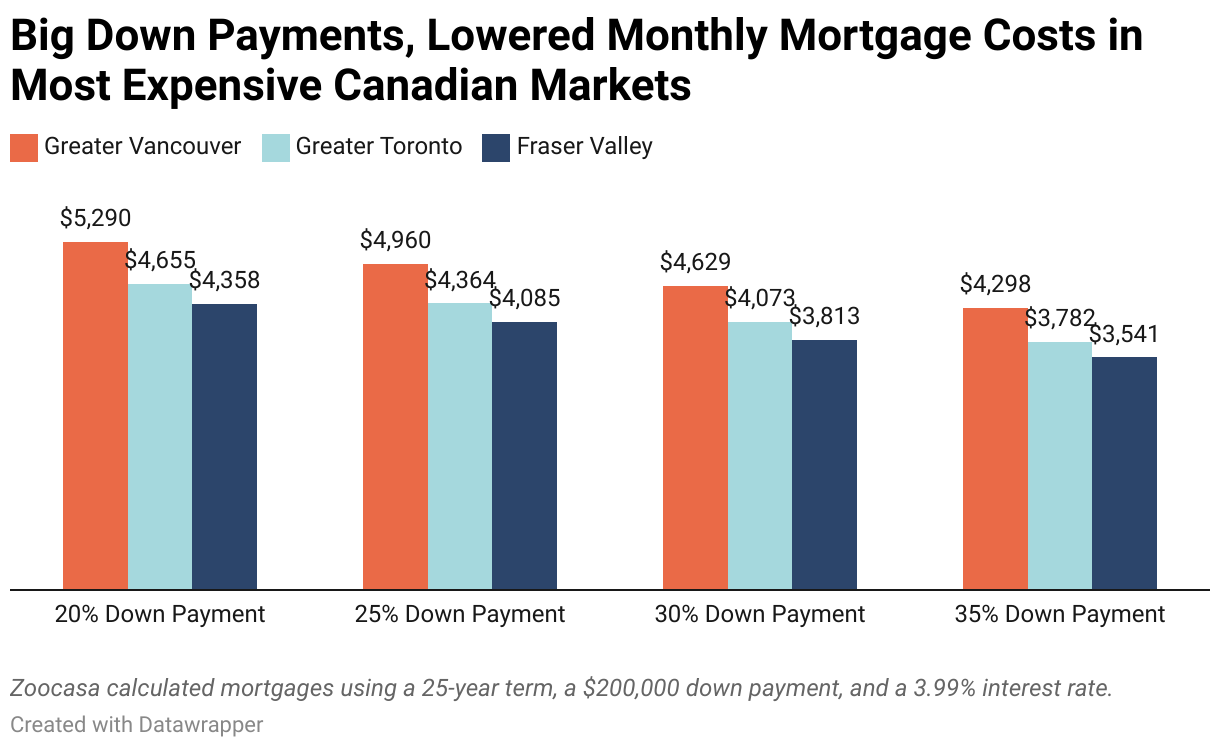

Even Canada’s most expensive markets benefit from a larger down payment. In Greater Vancouver, increasing down payments from 20% to 35% of the home’s cost lowers monthly payments by $992, saving nearly $12,000 annually. Similarly, buyers in the Fraser Valley save $817 monthly, while those in Toronto see a $873 reduction—adding up to $10,000 in yearly savings. Beyond easing immediate financial strain, these higher down payments significantly reduce long-term interest costs, making them a wise move for anyone eyeing these high-demand areas.

The Best Rental Markets for Millennial Investors

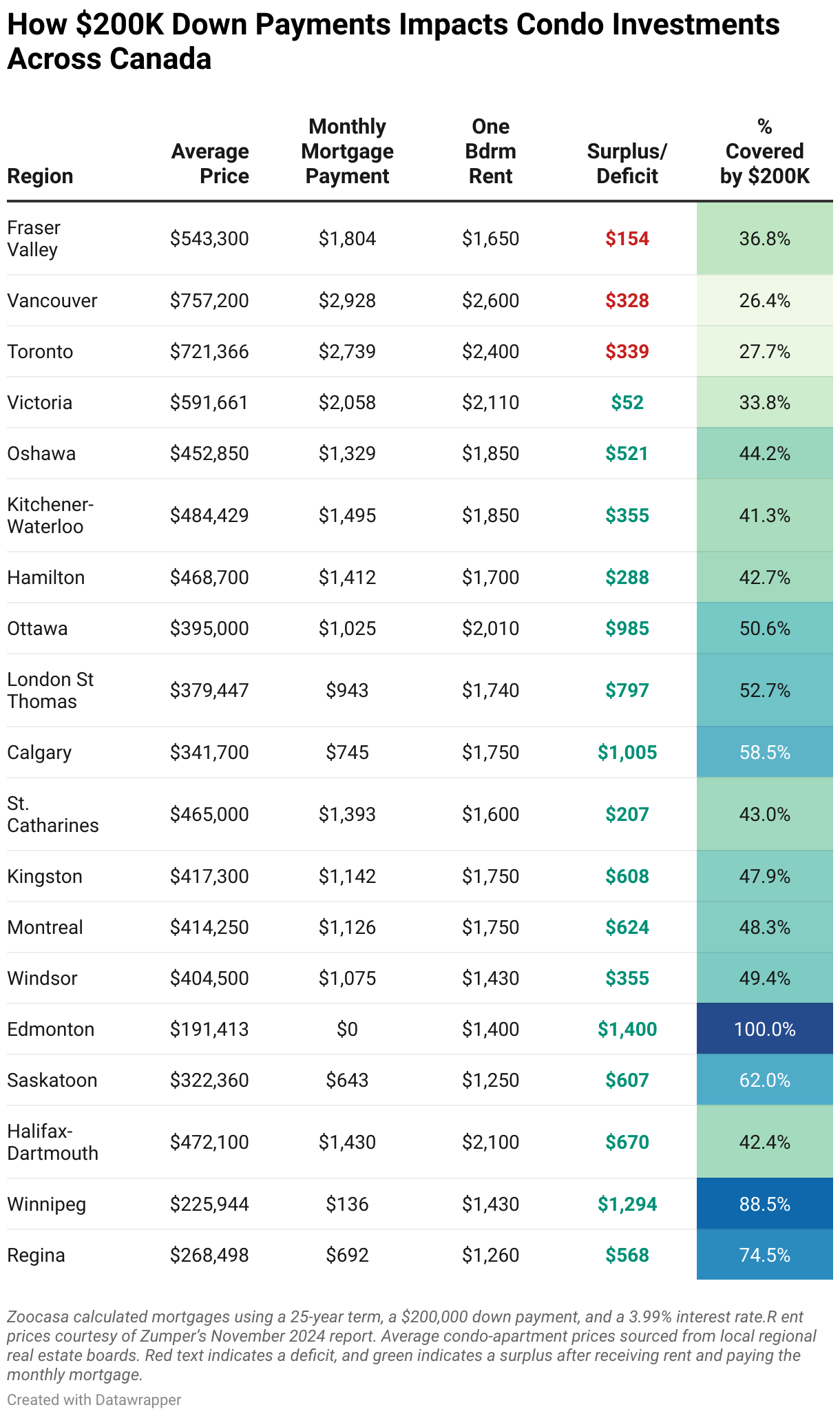

Rental markets also show promise for millennial investors, with nearly 58% of analyzed cities generating at least $500 more in rent than the monthly mortgage payment. Cities like Oshawa, Hamilton, and Kitchener–Waterloo deliver noteworthy value. With condo prices averaging $452,850, $468,700, and $484,429, respectively, a $200,000 down payment covers over 40% of the purchase price in each city. Monthly mortgage payments range from $1,329 in Oshawa to $1,495 in Kitchener-Waterloo, while average one-bedroom rental rates hover between $1,700 and $1,850. This surplus ensures steady cash flow and sets the stage for solid returns on investment.

With a $200,000 down payment in Ottawa, buyers can cover 50.63% of the average condo price of $395,000, leaving monthly payments at just $1,025. With average one-bedroom rents at $2,010, landlords enjoy a rental surplus of nearly $1,000 per month—an enticing proposition for anyone seeking consistent rental income.

Winnipeg takes affordability to the next level, with an average condo price of $225,944. Here, a $200,000 down payment covers 88.52% of the purchase price, leaving a minimal monthly mortgage payment of just $136. With average one-bedroom rents at $1,430, Winnipeg offers unparalleled cash flow potential.

Related: How Much Should Minimum Wage Be to Afford Rent Across Canada?

Invest Smarter: How Larger Down Payments Pay Off

Buying an investment property is a dream for many, but it comes with a hefty price tag in provinces like Ontario and British Columbia. With soaring home prices turning saving for a down payment into a marathon, parental support has become a critical factor in bridging the affordability gap.

In both Calgary and Edmonton, investors benefit from unique affordability advantages. Calgary’s average condo price of $341,700 allows a $200,000 down payment to cover 58.53%, resulting in monthly payments of $745. With rents averaging $1,750, landlords enjoy a surplus of over $1,000. Edmonton, where the average condo price is $191,000, stands out as an anomaly: a $200,000 down payment covers the entire purchase price, leaving buyers mortgage-free and generating 100% cash flow from day one.

The Macleans article notes, “Where housing is most expensive, the handouts are the highest, with Ontario and B.C. parents giving the most: $128,000 and $204,000, respectively.” This financial boost can make the difference between buying now or being priced out later. Still, it raises important questions about equity, opportunity, and the growing reliance on family wealth in Canada’s real estate market. As explained in the Macleans piece, according to Statistics Canada, nearly one in six homes owned by 1990s-born Canadians is co-owned with parents, and almost a third of first-time buyers receive family assistance for their down payments—trends especially pronounced in costly urban centers like Toronto and Vancouver.

Climbing Canada’s Most Challenging Real Estate Ladders

Parental support or inheritances can also reshape financial outcomes by enabling larger down payments, which offer significant advantages. Moving from a 20% to a 25% down payment requires a larger upfront investment—$62,923 in Greater Vancouver, $55,365 in Greater Toronto, and $51,829 in Fraser Valley—but it delivers significant monthly savings, reducing mortgage payments by $330, $291, and $273 respectively in these regions.

These larger down payments reduce long-term financial strain and decrease lifetime interest costs, strengthening financial security.

However, this growing reliance on family wealth highlights systemic affordability issues. The market increasingly favours those with access to intergenerational support while others struggle to compete.

The transformative period of wealth transfer creates unprecedented opportunities for millennials to enter the housing market or expand their investment portfolios. Whether it’s high cash flow in Winnipeg, long-term appreciation in Toronto, or affordability in Saint John, a $200,000 inheritance can reshape the real estate landscape for a new generation of buyers. With strategic planning, this windfall can lay the foundation for financial security and future wealth, ensuring millennials not only inherit money but also the means to grow it.

Do you have questions about buying or selling in your local real estate market? Our agents can help! Give us a call today to speak with an agent in your area and start planning your next real estate endeavor.