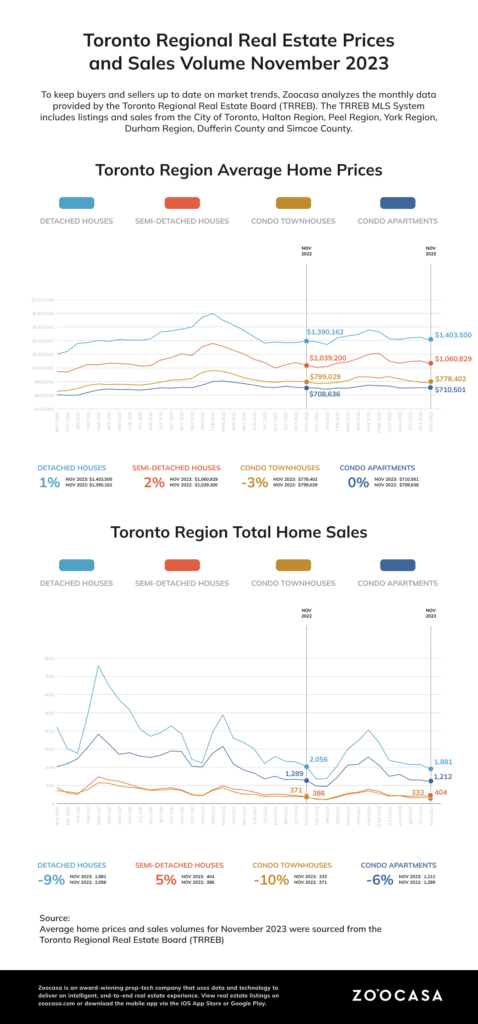

High borrowing costs and economic uncertainties persisted in November 2023, causing Toronto and Greater Toronto Area homebuyers and sellers to take another step back from real estate, influencing a year-over-year decline in home sales. The Toronto Regional Real Estate Board (TRREB) reported a 6% decline in sales year-over-year, but this sluggish state has allowed inventory to rebuild.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

The Bank of Canada’s last interest rate announcement of 2023 is scheduled for tomorrow and experts predict that we are edging closer to economic relief that will change the real estate market. “Inflation and elevated borrowing costs have taken their toll on affordability. This has been no more apparent than in the interest rate-sensitive housing market. However, it does appear relief is on the horizon. Bond yields, which underpin fixed rate mortgages have been trending lower and an increasing number of forecasters are anticipating Bank of Canada rate cuts in the first half of 2024. Lower rates will help alleviate affordability issues for existing homeowners and those looking to enter the market,” said TRREB President Paul Baron.

Growing Inventory Boosts Favourable Market Conditions for Buyers

This time last year, inventory was tight across major markets in Canada leading to difficult conditions for motivated buyers where sellers generally had the upper hand. In November 2023, TRREB reported that new listings increased 16.5% year-over-year. This has shifted market conditions and we recently reported that Niagara Region, the GTA, Hamilton-Burlington, and Victoria were buyers’ markets in October, while eight other major markets including London, Ottawa, and Greater Vancouver were in a balanced state. While many would-be buyers have taken to the sidelines awaiting improvements in affordability, inventory is rebuilding, leading to more stable market conditions and softening competition.

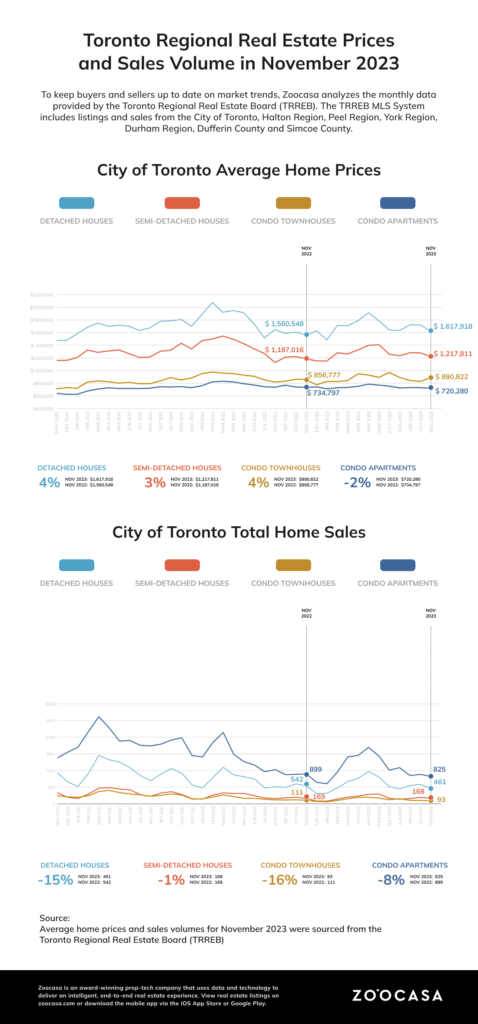

Home Prices Have Flattened Across the GTA

The average home price was $1,082,179 in November 2023, a marginal increase of 0.26% from the average price of $1,079,420 in November 2022. The average price in some of the most in demand local markets have dipped below the $1 million mark. In November 2023, Mississauga’s average home price fell to $993,352, a 10% decrease month-over-month with the biggest decline in price in the detached sector, now sitting at an average price of $1,398,829, a 10% decline month-over-month.

Year-over-year, the average detached home price has increased by just 0.8%, while condo apartment prices have remained the most flat, increasing by just 0.4%. The average townhouse price has decreased year-over-year in both the 416 and the 905, down by 3.6% and 0.7% respectively.

“Home prices have adjusted from their peak in response to higher borrowing costs. This has provided some relief for buyers, from an affordability perspective. As mortgage rates trend lower next year and the population continues to grow at a record pace, expect demand to increase relative to supply. This will eventually lead to renewed growth in home prices,” said TRREB Chief Market Analyst Jason Mercer.

Preparation is Key in Shifting Economic Landscapes

Prospective buyers are growing tired of sitting on the sideline and putting off their home-buying plans. As we continue to inch towards anticipated Bank of Canada rate cuts, Canadians need to prepare effectively and closely monitor the economic climate as well as their financial situations. We learned during the pandemic that market conditions can shift quickly and interest can be reignited overnight.

Our real estate agents are in your city and available to help you prepare. Whether you have questions about today’s market or are looking for more information about when the right time for you to buy is, contact us today for more information.